Per some reports, nearly 6 in 10 users drop off during onboarding when asked to manually enter bank details or wait for verification to complete. That’s a massive hit, not just to conversion rates, but also to trust.

While users want speed, businesses want certainty. And in between, traditional verification methods often fall short. But today, forward-thinking platforms are reimagining how verification works, making users a part of the process, not just passive recipients.

Instead of sending a token amount to check validity, what if the user sent one? That small shift is solving big problems, from fraud prevention to faster onboarding.

In this blog, we dive into what reverse penny drop is, what it means, how it works, and why it’s changing the way digital businesses verify bank accounts.

Traditional penny drop vs. reverse penny drop

Regardless of whether it’s a first salary payment, insurance payout, or refund from an online marketplace, businesses must verify the bank account details of a customer before processing the transaction.

But when it comes to token-based verification, should they stick with the penny drop method or move to reverse penny drop?

After all, both methods are widely used for account verification, and each comes with its own set of advantages and trade-offs.

Let’s take a closer look.

1. Traditional penny drop method:

In the traditional penny drop method of bank account verification, a business deposits a small amount, usually ₹1, into the user’s bank account. This transaction confirms the active status of a bank account and ensures that you have the right account details.

Once the transaction is successful, the business receives a response from the bank (via API) that typically includes the account holder’s name. This name is then compared with the name entered by the user during onboarding to check for a match. If it matches, the account is verified.

While the method is widely adopted, it has a few limitations:

- It doesn’t confirm the user identity, i.e., who owns or controls the account

- The bank’s name response is capped to 20 characters (for most APIs), which can lead to name mismatches and failed verification

- It requires a user to manually enter bank details like account number and IFSC code, increasing the chances of manual errors, not to mention drop-offs

- It facilitates unauthorized transactions if incorrect or third-party account details are submitted

Despite this, the penny drop remains a go-to method for many businesses to verify borrowers’ bank accounts. It’s simple, moderately secure, and fits well into existing systems.

Read more: 15+ Documents Required for Opening A Bank Account

2. Reverse penny drop method

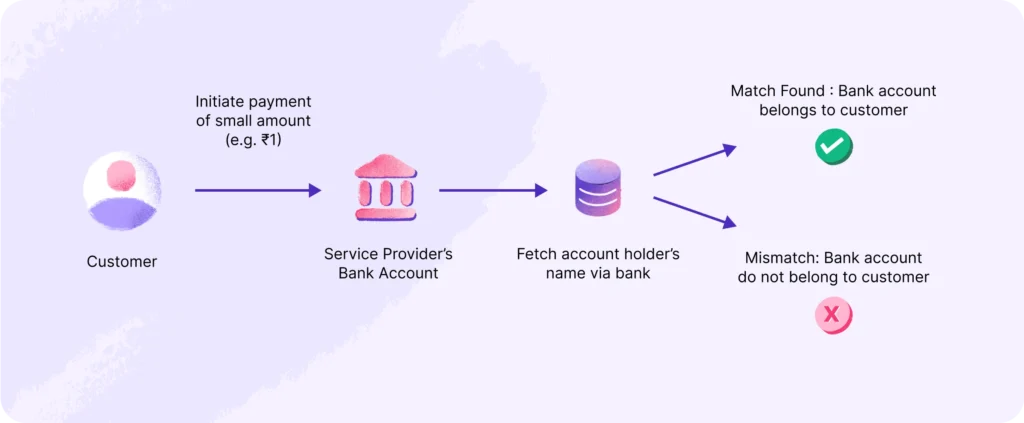

Reverse penny drop(RPD) is a user-initiated instant bank account verification method. Here, the user makes a small payment, typically ₹1, to the business’s account using their preferred UPI app.

Unlike traditional penny drop, where the business sends money to verify an account, reverse penny drop shifts the onus to the user. Since the payment is made directly from the user’s own bank account, it serves as strong proof of ownership.

This method requires no manual input from the user–no account number, no IFSC code, and no scanned documents. Once the business receives the payment, it can extract the user’s bank account details, including the account number, account holder name, and IFSC code, through the UPI rails.

After verification, the amount is refunded to the user automatically. And the entire process takes no more than a couple of seconds.

The only caveat? RPD account verification processes can only be used by regulated entities.

Comparative analysis

Let’s now compare the penny drop and reverse penny drop methods, side-by-side, to verify the bank account details of a user.

| Feature | Penny drop | Reverse penny drop |

| Transacting party | Business pays ₹1 to the user | The user pays ₹1 to the business |

| Input required | Requires the customer’s bank account number and IFSC code | Requires no input |

| Output generated | Upon transaction, the business receives the customer’s bank account name | Upon transaction, a business receives the customer’s bank account name, number, IFSC code, and UPI ID |

| Drop offs | High users drop off as they are required to manually enter details about the account number and IFSC | Since the entire process requires zero input from customers, drop-offs are low |

| Failure | Manual errors like incorrect account details and IFSC can cause failure | Since there’s no manual input, there’s no room for errors |

| Financial fraud and scams | Siphoning and fake account identities can cause significant financial losses to a business | Foolproof verification method with no scope for fraud or account takeover |

| Use case | Works in systems where businesses want to verify accounts passively | Ideal for apps requiring active user consent and faster KYC workflows |

| Fund recovery | ₹1 stays with the beneficiary account (user) and is not refunded to the business | ₹1 is refunded to the user after verification |

Benefits of reverse penny drop

Reverse penny drop has seen rapid adoption across fintechs, lenders, and platforms that rely on real-time bank account verification. It addresses many core issues businesses face with traditional methods, especially around security, accuracy, document verification, and drop-offs.

Here’s how reverse penny drop benefits the business:

- Enhanced security

Unlike traditional penny drop, where the system accepts whatever account details are entered, reverse penny drop makes it nearly impossible to verify a third-party or fraudulent account.

This is because the user initiates a transaction using their own UPI app, which is already linked to their verified bank account. This simple act adds a critical security layer. Only someone with access to the user’s device, UPI pin, and bank account information can complete the process.

- Reduced fraud risk

Since reverse penny drop requires the user to send money from their own bank account, it provides direct proof of ownership. This prevents scenarios where someone tries to link an account they don’t actually control.

It helps stop fraud like:

- Money laundering, where third-party accounts are used to route illegal funds

- Users entering someone else’s bank account just to get through verification

- Adding fake beneficiary accounts to steal payouts or refunds

- Using the same account to create multiple fake user profiles

- Faster verification process

The bank account verification through the reverse penny drop API happens in real time. Not minutes but seconds.

As soon as the user makes a ₹1 UPI payment, the system extracts their bank account details instantly. Most verifications are completed within seconds, leading to a smoother user experience and streamlined customer onboarding.

- Cost-effectiveness

RPD is fully automated with over 95% success rates. It reduces the need for manual checks, follow-ups, or handling of failed transactions. It also eliminates costs tied to user errors, incorrect account details, and re-verification loops that are common with traditional verification methods.

Meaning businesses don’t need large support teams to manage account verification processes.

How does reverse penny drop work?

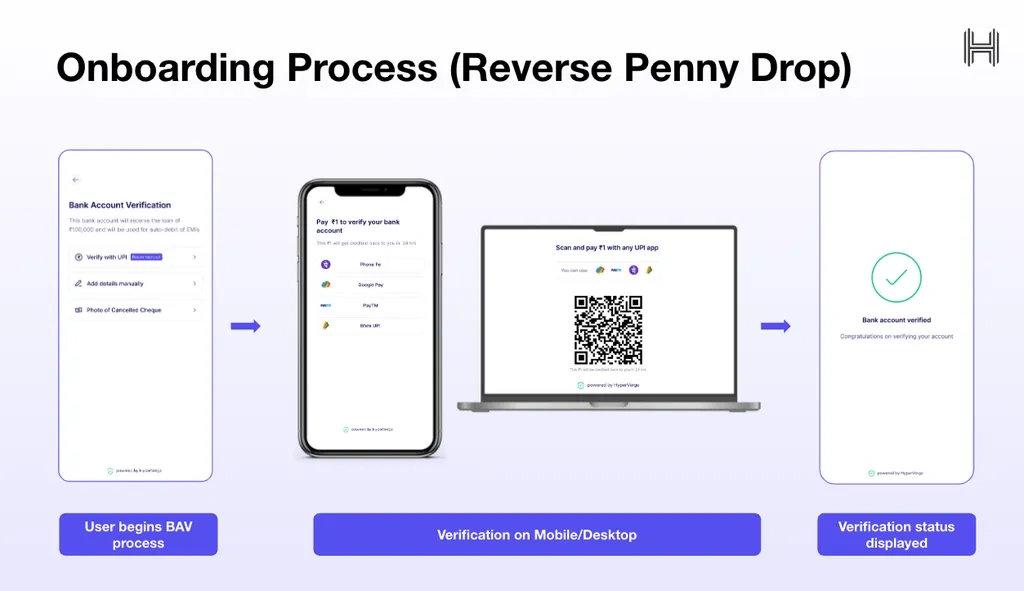

Here’s a step-by-step process explaining how user-initiated reverse penny drop verification/UPI-based verification works with HyperVerge:

- The user reaches the ‘Bank Account Verification’ step within the platform’s app or website while completing onboarding

- The user selects the ‘Verify with UPI’ option (Reverse Penny Drop method) to start the verification. They can choose between PhonePe, Google Pay, BHIM UPI, or Paytm to pay ₹1 to the business

- The user completes the transfer by entering their UPI PIN on their mobile or desktop

- Once the payment succeeds, the system fetches the account holder’s name, account number, and IFSC via UPI rails and verifies the bank account

- The user instantly sees a screen that shows the real-time verification status

The entire flow completes within a couple of seconds, making it quick and efficient for users.

Challenges in current systems and solutions

Even with automation, many businesses still face friction in their bank account verification processes. Why so? Mainly because of infrastructure challenges, software inefficiencies, and a lack of fallback mechanisms.

Let’s discuss a few challenges with current systems along with solutions to overcome them.

High-user drop-offs

Penny drop verification is still the go-to method for many nonregulated entities. But the problem isn’t the method, it’s how users are asked to complete it.

Asking users to manually enter their IFSC code or search for the bank name often leads to mistakes and drop-offs. Users may lack the time and patience to go back and forth for a simple verification.

Solution: Choose a tool with an enhanced interface, like HyperVerge one that supports bank and IFSC search, auto-fill suggestions, and real-time input validation. Also, implement a fallback workflow. If verification via penny drop fails (due to invalid inputs or bank API issues), automatically trigger a retry with corrected details or switch to a manual review.

No visibility on conversions

Most verification systems don’t offer real-time insights into how many users complete the flow, where they drop off, or why verification fails. This makes it hard for teams to track performance or fix broken steps.

Solution: HyperVerge offers an interactive analytics dashboard helping you analyze success/failure rates for different methods, verification times, and even friction spots in the account verification journey. It helps you make data-backed improvements to your workflow so that no user leaves the verification process in between. Also, HyperVerge’s RPD has a success rate of 97%, and its penny drop verification garners 94% successful conversions with zero downtime.

High effort and TAT for integration

Setting up bank account verification, especially reverse penny drop APIs, can take significant time, in some cases, even months. This is due to complex flows, regulatory dependencies, and coordination with multiple partners.

Solution: Choose HyperVerge’s end-to-end solution with a single SDK integration that gives you access to multiple verification methods in India, i.e., penny drop, penniless, RPD, IFSC, and cancelled cheque OCR. What’s more? It lets you build custom journeys, switch between methods like penny drop and reverse penny drop, and implement fallback logic, all without managing multiple APIs or service providers.

Future of reverse penny drop in India

Reverse Penny Drop (RPD) is quickly becoming the preferred choice for verifying bank accounts in India, and its future looks strong; in the same context, HyperVerge predicts:

- UPI auto-debit may be layered in, letting platforms verify the account and set up mandates in one flow

- Pennyless bank account verification

- AA + RPD will likely converge, allowing platforms to confirm account ownership and pull financial data with user consent

- RPD adoption will expand beyond non-regulated entities, easing onboarding for all sorts of businesses

HyperVerge is at the forefront of this shift. Its bank account verification suite supports penny drop, penniless, and reverse penny drop, all through a single SDK for web and mobile.

What’s more? HyperVerge’s built-in analytics and workflow tools give you granular control and help you track and optimise drop-offs across your onboarding journeys.