Are your payments really reaching the right bank accounts, or are you just hoping they do?

For India, which processes billions of digital payments each year, financial fraud remains a rising threat. According to a recent report, India lost over ₹11,000 crore to cyber fraud in just the first nine months of 2024!

To counter such threats, Bank Account Verification (BAV) is no longer an optional feature; it’s a critical layer of defense against fraud, error, and non-compliance.

But how to choose a BAV solution amidst a sea of viable options? This guide breaks down BAV solutions in India, helping you choose one that’s not just secure but smart, designed to adapt, scale, and simplify your operations.

Understanding Bank Account Verification (BAV)

Bank Account Verification (BAV) is the process of confirming the legitimacy and ownership of a bank account. It’s conducted by cross-referencing details such as account numbers, names, bank branches, and identification documents against official records. This verification ensures that transactions are conducted securely, reducing the risk of fraud, errors, and financial mismanagement.

Importantly, BAV ensures compliance with regulatory frameworks such as Know Your Customer (KYC) and Anti-Money Laundering (AML). This makes it a mandatory step in various financial operations.

Common use cases of BAV in India

Several types of BAV are widely used across industries to verify financial details and ensure secure transactions. Here are some of its key applications:

- Onboarding new customers: Banks and fintech companies verify account details before allowing transactions

- Processing vendor or employee payments: Businesses confirm bank account details to ensure salary and supplier payments reach the correct accounts

- Facilitating refunds and reimbursements: E-commerce platforms and financial service providers verify accounts before issuing refunds to minimize transaction failures and fraud

By implementing a reliable BAV solution, businesses can enhance security, streamline payments, and maintain compliance with ease.

Read More: Key Terms for Bank Account Verification in India

Key factors to consider when choosing a BAV solution

Selecting the right BAV solution requires a careful assessment of many factors, ranging from verification methods to security and integration capabilities.

Here are some key aspects to evaluate:

Verification methods offered

Not all verification methods are created equal. Moreover, what works for a small business may not be suitable for enterprises handling large volumes of transactions. Some of the most common BAV methods include:

- Manual Document Verification: As the name suggests, this method includes manually collecting and validating the user’s details using a cancelled cheque, passbook copy, bank account statement, or address proofs

- Penny Drop (Micro-Deposit): A small amount is deposited into the recipient’s bank account. Verification is done by confirming the credited amount. This method is reliable but may be slow for high-volume transactions

- Reverse Penny Drop (RPD): In this method, the recipient initiates a small payment, typically ₹1, via UPI to the verifying entity. Once details are verified, the amount is refunded

- Pennyless Verification: In this method, the user’s bank account details are validated without any transactions

- Cancelled Cheque OCR: This method requires the recipient to upload a cancelled cheque, from which all appropriate details are automatically extracted

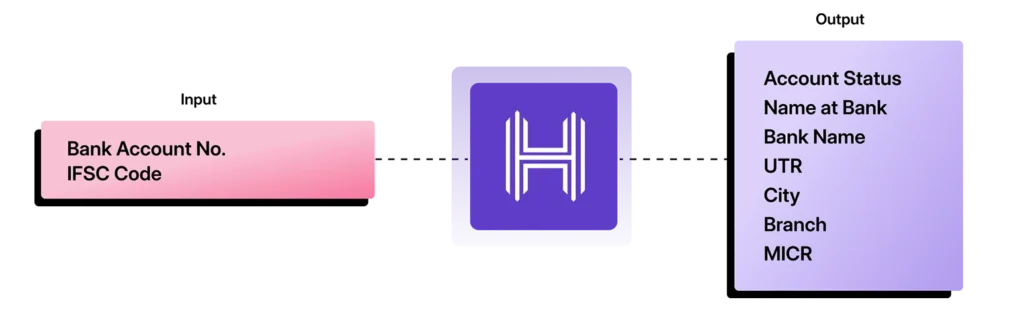

- IFSC Verification: This method fetches the bank address, name, and other details using the IFSC code for more accurate routing of funds

- Aadhar Verification: This method uses the user’s Aadhaar details to verify whether it’s linked to an active bank account

Assess your business needs in terms of scale, frequency, and urgency to determine the most suitable verification method.

Accuracy and reliability

A digital BAV solution must deliver precise and error-free verification. Even minor discrepancies in account details can lead to transaction failures, payment delays, or compliance issues.

Opt for a solution that cross-checks data against many sources to ensure high accuracy.

Integration capabilities

A good BAV solution should seamlessly integrate with the existing payment systems, CRMs, or ERP platforms. API-driven solutions are particularly beneficial as they enable automated verifications without disrupting workflows.

Compliance and security

Given the strict financial regulations in India, a BAV solution must follow KYC, AML, and RBI guidelines. Additionally, robust data encryption and security protocols are non-negotiable.

User experience

The ease of use for both businesses and end-users is a crucial factor. A cumbersome verification process can lead to delays, errors, and poor customer experiences. Choose a solution with a simple, intuitive interface and minimal manual intervention.

Cost-effectiveness

BAV solutions come with different pricing models–per-transaction fees, subscription plans, or enterprise pricing. Ensure that the solution aligns with your budget while maintaining the quality, speed, and security necessary for your operations.

By carefully evaluating these factors, businesses can select a BAV solution that not only enhances security and compliance but also streamlines customer onboarding and improves user experience.

Read More: What Is Instant Bank Account Verification And Why Is It Important

Benefits of implementing an effective BAV solution

A well-executed BAV solution does more than just confirm account details. It strengthens financial security, enhances operational efficiency, and builds trust with customers. Here’s how:

1. Fraud prevention

India has seen a steady rise in financial fraud cases. From unauthorized transactions to identity theft, money crimes are quite prevalent. A robust BAV solution acts as the first line of defense by verifying that an account belongs to the person or organization claiming ownership.

This reduces the risk of fraud such as fake identities, account takeovers, and fund misdirection. By detecting discrepancies early, businesses can prevent costly fraud incidents before they occur.

2. Operational efficiency

Manual verification methods can be time-consuming and error-prone. Practices like reviewing bank statements and all other documents required to open a bank account can be inefficient. Automating the BAV process eliminates these inefficiencies, allowing businesses to:

- Reduce manual intervention: Automated verification ensures faster onboarding and transaction processing

- Minimize errors: Incorrect account details or manual data entry mistakes can lead to failed payments. A digital BAV solution significantly lowers this risk

- Improve scalability: For businesses handling high transaction volumes, automation ensures smooth operations without bottlenecks

By integrating an efficient BAV system, companies can speed up financial processes, reduce costs, and improve overall productivity.

3. Enhanced customer trust

Even minor errors in bank account details can lead to failed transactions, frustration, and a damaged reputation. Secure and seamless verification reassures customers that their funds are protected. This further strengthens their confidence in a business. For instance, think of how India’s top UPI apps offer seamless transactions.

Besides user-friendly interfaces, BAV also offers robust back-end verification processes, thus ensuring secure payments. When customers trust that their transactions are safe, they’re more likely to remain loyal, driving business growth.

Steps to implement a BAV solution

Adopting a BAV solution requires a structured approach to ensure efficiency, compliance, and security. Here’s how businesses can successfully implement the right solution:

1. Identify business requirements

Before selecting a BAV solution, businesses must define their specific needs. This includes assessing transaction volumes, the required level of automation, and compliance obligations.

For instance, enterprises handling high transaction volumes may need real-time verification. Meanwhile, smaller businesses may prioritize cost-effective options. Understanding these requirements helps in selecting a solution that aligns with operational goals.

2. Research and shortlist providers

With various BAV solutions available, businesses should research providers based on key factors. These entail verification methods, industry reputation, and adherence to Indian financial regulations. Additionally, ease of integration with existing systems is crucial.

Shortlisting providers that match these criteria ensures that the chosen solution can meet operational demands efficiently.

3. Request demos and trials

Before finalizing a provider, businesses should ideally engage with shortlisted vendors for product demonstrations and trial periods.

A live demo provides insights into the verification process, while trial periods allow businesses to evaluate real-world performance. This hands-on approach helps in making an informed decision.

4. Evaluate and select

After testing different solutions, businesses must compare them based on critical factors such as accuracy, scalability, security compliance, and cost-effectiveness.

The right solution should minimize verification errors and seamlessly handle high transaction volumes. Besides, it must follow RBI guidelines, KYC, and AML requirements. Choosing a solution that balances efficiency with affordability ensures long-term success.

5. Integration and training

Once a BAV solution is selected, businesses must integrate it with their existing financial systems.

A seamless API integration can automate verification processes, reducing manual effort. Additionally, training staff on how to use the solution effectively is essential to avoid errors and optimize efficiency. Continuous monitoring and performance assessments help ensure smooth operations and quick resolution of any issues that arise.

Key takeaways

The right BAV partner doesn’t just protect your business, it powers it.

With the rise of digital payments and financial fraud, businesses must prioritize accuracy, security, and seamless integration when choosing a BAV provider.

That’s where HyperVerge’s BAV solution stands out. Built for scale and speed, the platform offers real-time validation, razor-sharp accuracy, and effortless integration with your existing systems. From Pennyless Verification to Reverse Penny Drop and Cheque OCR to IFSC lookups, we provide every mode of verification under a single, seamless SDK.

If you’re looking to future-proof your payment infrastructure without leaving any room for guesswork, HyperVerge’s end-to-end BAV platform is ready to deliver.

Book a demo today!