Every failed payout, delayed salary, or fake beneficiary entry adds cost and risk. For fintech apps disbursing microloans, NBFCs onboarding gig workers, or payroll teams processing thousands of salaries, speed and precision in verifying bank accounts are non-negotiable. Penny drop methods fall short: they require ₹1 deposits, introduce latency, and still leave room for fraud.

Pennyless verification changes that. It uses secure APIs to instantly confirm the account holder’s name and validity without sending a single rupee. This cuts drop-offs, eliminates delays, and helps platforms go live with verified users in seconds. As fraud becomes more sophisticated and compliance becomes tighter, this real-time method is becoming the backbone of modern financial workflows in India.

If you’re new to pennyless verification, this blog is the right place to start. It covers every aspect of it, including definition, benefits, process, and explores HyperVerge’s pennyless verification API.

What is Pennyless Verification?

Pennyless verification is a modern solution that streamlines the process of validating bank accounts. But before we go further, let’s understand the difference between pennyless and penny drop to avoid confusion.

Pennyless verification validates bank account details without transferring money—that’s how it gets its name, “pennyless.” It uses the account number and the IFSC code to confirm the account’s legitimacy with the bank’s records. In a penny drop verification, a nominal amount (typically Rs.1) is deposited into the bank account to verify its validity.

Fintech companies and businesses prefer pennyless verification due to its speed and efficiency, low transaction cost, and enhanced security.

Pennyless vs. Penny Drop Verification

The verification process is the principal difference between pennyless and penny drop, which we have already covered in the last section. Here are three more differences with a use case:

| Pennyless Verification | Penny drop Verification | |

| Speed | Pennyless verification is faster. No time taken for fund transfers and reconciliation | Penny drop verification may face delays due to interbank transaction processing times |

| Cost | Pennyless verification is more cost-effective because there are no transaction charges | Penny drop verification incurs transaction fees for each verification |

| User experience | Pennyless verification provides a seamless experience by avoiding such transactions | Penny drop verification can confuse users due to unexpected deposits, raising concerns about fraud |

| Use case | Pennyless verification is perfect for high-volume merchant onboarding where speed and cost efficiency are critical. | Penny drop verification is ideal when the platform requires a financial transaction as part of the process. For example, if an e-commerce platform wants to test the payout mechanism by depositing ₹1 into a customer’s account |

Invest in a pennyless verification solution

trusted by 350+ companies across 295 countries Schedule a DemoWhy Businesses Need Pennyless Verification?

Pennyless verification offers several advantages to overcome the challenges fintech professionals face. For example, compliance requirements, which 93% of the fintechs reportedly struggle with. Let’s explore these advantages in more detail in this section.

Instant and Cost-Effective Verification

Pennyless verification reduces transaction costs compared to the traditional penny drop method. For example, a payment gateway onboards thousands of merchants each month. With penny drop verification, each small transaction incurs fees, adding up significantly over time. By switching to pennyless verification, these businesses can eliminate those costs while still ensuring accurate account validation.

Moreover, instant validation bolsters quick onboarding, which is a great way to begin a solid and long-term customer relationship. This is especially true for fintech apps that promise users immediate access to funds upon account setup.

Enhanced Fraud Detection

Over 25% of banks and fintechs reported losses exceeding $1 million, and their consumers faced cumulative losses of more than $10 billion due to fraudulent activities. In addition to monetary loss, fraud leads to reputational damage and derails operations in fintech institutions.

Pennyless verification is critical in identifying fake or dormant accounts before any transactions occur. For instance, if a user attempts to register with a fictitious account number, the system can flag this immediately through direct validation with the bank’s database.

Compliance with Regulatory Standards

The Reserve Bank of India (RBI) and National Payments Corporation of India (NPCI) mandate strict KYC norms for banks and financial institutions. As per the RBI’s updated KYC guidelines (effective November 2024), financial institutions must verify customer details using reliable sources. Similarly, the NPCI emphasises seamless identity verification through biometric and OTP methods.

Pennyless verification supports these norms by validating bank account ownership and status without relying on monetary transactions and confirming account legitimacy without disclosing sensitive information like Aadhaar numbers.

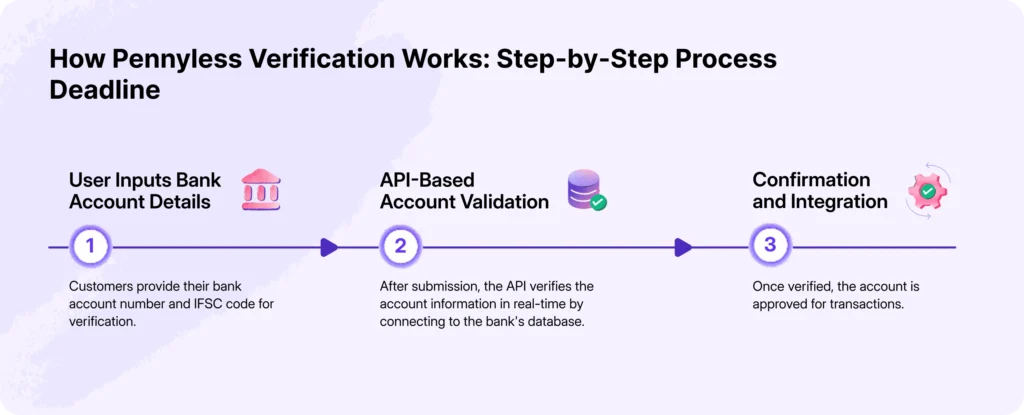

How Pennyless Verification Works: Step-by-Step Process

Here’s a simple breakdown of the steps involved in pennyless verification. This will be useful if you’re planning to implement the process in your organisation:

Step 1: User Inputs Bank Account Details

The process begins with customers providing their bank account number and IFSC code for verification.

Step 2: API-Based Account Validation

After the user provides their details, a secure Application Programming Interface (API) runs in the background. This API verifies the provided account information in real-time by connecting directly with the bank’s database.

Step 3: Confirmation and Integration

Once the account is verified, it is approved for transactions or further processing. With this seamless integration, businesses can proceed with onboarding without delays, ensuring a smooth user experience.

Benefits of Pennyless Verification for Businesses

Are you wondering if penniless verification is not the right fit for your business? These three benefits might help you change your mind.

Fast and Seamless Customer Onboarding

A complicated onboarding process drives away 7 out of 10 customers. In the fintech space, where customers have multiple options, your onboarding must be smooth and quick. One way to improve your current onboarding steps is to use pennyless verification. This method enables instant account validation and reduces friction in digital KYC processes.

For example, a lending platform can quickly onboard borrowers and provide instant access to funds. This speed enhances customer satisfaction and minimises churn.

Cost Savings Compared to Traditional Methods

The traditional penny drop verification costs a penny to validate an account. It’s not significant when you consider verifying a single account’s identity. But when you increase the volume 1000X, the total blows up and becomes significant.

For instance, if a company verifies 10,000 accounts monthly at ₹1 per transaction, they save ₹10,000 every month by switching to pennyless verification. This cost efficiency is especially beneficial for large enterprises managing high volumes or startups operating on tight budgets.

Scalability for Large Enterprises and Startups

When you scale your business and onboard more customers, you want the KYC process to be the same, quick, and secure. Pennyless verification supports growing operational demands, like onboarding thousands of customers daily. It works the same way without putting much pressure on your existing infrastructure, which is excellent news for your growing business.

How to Choose the Best Pennyless Verification Solution?

You must pick the right solution to set up a pennyless verification process in your organisation. Here are the four parameters to evaluate the right solution.

Speed and Accuracy

Prioritise solutions that offer real-time validation capabilities with minimal errors. The ability to instantly verify account details is necessary for quick customer onboarding and operational efficiency. Also, a solution with a high accuracy rate reduces the risk of false positives and negatives, i.e. only legitimate accounts are validated swiftly while fraudulent ones are flagged.

Compliance and Security Features

Compliance is a non-negotiable factor when you evaluate a pennyless verification solution. Adhering to RBI guidelines by complying with the KYC and AML regulations will avoid legal repercussions. Moreover, look for robust security features like data encryption and secure access controls to protect sensitive customer information from breaches, fostering trust in your services.

Integration Capabilities

Choose a solution with seamless API integration to work with existing banking and fintech platforms. A well-designed API enables smooth system communication for efficient data exchange and streamlined workflows.

Fraud Prevention Mechanisms

Give preference to solutions with AI-driven risk detection mechanisms. AI can analyse patterns and behaviours in real time, identifying potential fraud. As it uses machine learning algorithms, your organisation can stay one step ahead of fraudsters, ensuring safer transactions and protecting both your business and customers.

HyperVerge’s Pennyless Verification Solution

HyperVerge’s pennyless verification solution stands out as a robust, AI-driven tool designed to meet the needs of bank account verification. Here’s how HyperVerge delivers exceptional value:

AI-Powered Fraud Detection

HyperVerge leverages advanced AI models to detect suspicious activities in real-time. These models analyse patterns and behaviours to flag anomalies, such as fake or dormant accounts, before they can disrupt operations. For example, the system can identify discrepancies in account ownership details, preventing fraudulent transactions and safeguarding businesses from financial losses.

Secure API Integration

HyperVerge offers a plug-and-play API integration, which means you can go live quickly, ensuring faster time-to-market and operational efficiency. Beyond the pennyless verification API, HyperVerge also supports diverse bank account verification needs to meet specific business use cases. These include the bank account verification API, which validates accounts through nominal fund transfers, and the reverse penny drop verification API, which retrieves account details without initiating a transaction.

HyperVerge’s APIs have automated fallback mechanisms to ensure uninterrupted service during system downtimes and reduce user drop-offs. The built-in analytics also empowers companies to optimise workflows and deliver a seamless user experience continuously.

Instant Verification with High Accuracy

HyperVerge’s pennyless verification is based on instant bank account verification, which means a user’s bank account details are verified within seconds. It directly connects to bank databases, enabling faster customer onboarding, and with a high accuracy rate, it presents a superior user experience.

Future of Pennyless Verification in India

The adoption of pennyless verification is set to grow rapidly as financial institutions increasingly recognise its efficiency and cost-effectiveness. India’s digital payments market is projected to reach $123 billion by 2030. Banks, fintech companies, and businesses will need secure and scalable account verification methods to keep up with this growing market. The streamlined approach of pennyless verification aligns with the growing demand for faster onboarding and fraud prevention in the financial ecosystem.

Additionally, the development of advanced AI models is shaping the future of pennyless verification. These models will enhance the fraud detection capabilities and ensure real-time identification of suspicious activities. As India continues to embrace cashless transactions and digital banking, pennyless verification will play a key role in ensuring trust, compliance, and operational efficiency across the financial sector.

Key Takeaways

Pennyless verification is a modern solution for banks and financial companies to improve efficiency and security. Here’s a quick summary on how it helps:

– It eliminates the need for monetary transactions and simplifies the verification process.

– This transformation accelerates the onboarding experience and aligns with the increasing expectations of tech-savvy consumers.

– Businesses also benefit from pennyless verification through fraud-resistant account validation, which protects businesses from potential losses

In summary, penniless verification is an essential asset for companies looking to enhance their operational efficiency while balancing customer trust and regulatory compliance.

FAQs

1. What is pennyless verification, and how does it work?

Pennyless verification is a modern account validation method that confirms a bank account’s identity without transferring any funds. It verifies the account number and IFSC code directly with the bank’s database using secure APIs. This process ensures real-time validation of account details, including the account holder’s name and status, offering a faster and more efficient alternative to traditional methods

2. How is it different from penny drop verification?

Penny drop verification involves transferring a nominal amount (Rs. 1) to validate account details. Pennyless verification, on the other hand, eliminates monetary transactions entirely. While Penny Drop requires confirmation of deposits, Pennyless verification uses advanced data validation techniques to verify account information directly. Therefore, it is faster, more cost-effective, and less prone to user confusion

3. Why is pennyless verification important for businesses?

Pennyless verification addresses critical business needs such as reducing transaction costs, accelerating customer onboarding, and enhancing fraud prevention. It also ensures compliance with regulatory standards like KYC and AML while streamlining operations.

4. Which industries benefit the most from pennyless verification?

Banking, fintech, payroll processing, lending platforms, and e-commerce industries will benefit significantly from pennyless verification. For example, payroll companies can validate employee accounts efficiently, while fintechs can onboard customers faster without compromising security and reducing costs.

5. How can I integrate a pennyless verification solution into my business?

You can integrate a penniless verification solution like HyperVerge with secure API-based systems. These APIs function on a simple plug-and-play basis, meaning you can incorporate the service into your workflows seamlessly. They also support automated fallback mechanisms and built-in analytics to optimise onboarding processes.