In the digital era, new account fraud—where fraudsters establish fictitious accounts using a stolen identity or synthetic identities to target financial institutions, fintech companies, and e-commerce businesses—is an increasing danger.

Your money could be taken through this false account, your reputation might suffer, and even legal consequences could result. This is the reality of new account fraud, a rising concern for companies handling online sales.

Preventing fresh account fraud is crucial for protecting your company from financial losses, damage to reputation, and legal fines.

Let’s explore new account fraud in detail, along with the several forms of account takeover fraud you should be aware of and, most significantly, how to stop it from happening in your company.

What is new account fraud?

New account fraud or account origination fraud, is the creation of false accounts meant for financial crime execution. Fraudsters use fake or stolen identities (synthetic identity fraud) or even steal your identity (identity theft), surpassing the security of your system. These fraudulent accounts let them launder money, make unauthorized purchases, acquire unlawful items, or even steal money.

Types of new account fraud

There are various types of financial fraud and new account opening fraud, and fraudsters use a wide variety of strategies. A few of the most prevalent kinds are listed below, along with descriptions of their operation and warning signs to anticipate:

Identity theft and synthetic identity fraud

Theft of personal information: Under this scheme, cybercriminals take actual people’s personal details such as names, SSNs, addresses, and even anniversary dates. Based on this stolen information, they will create fake accounts in your system. Because these accounts could seem real at first glance, they are hard to track down.

Keep an eye on account fraud work and out for discrepancies in client data, like duplicate phone numbers or street addresses. Accounts created using freshly issued Social Security numbers or from nations with a high fraud rate should raise red flags.

Synthetic identity fraud: In synthetic identity fraud, criminals create fake identities using a combination of real and fictitious information. As an illustration, they may use a genuine name while fabricating their address and Social Security number. Since they might not raise any obvious warning signs, these fake documents and identities are trickier to uncover than stolen ones.

Synthetic identity fraud may be present if unusual combinations of personal information are present, such as a young individual with a lengthy credit history. Keep an eye out for accounts that don’t have much of a credit history or financial accounts that use anonymous funding, such as prepaid credit card accounts.

Account takeover and account farming

Account takeover: Scammers commandeer existing bank accounts by using techniques like phishing and malware or by buying stolen credentials on the dark web. Their actions can escalate to identity theft, fraudulent purchases, and fund theft once they have access to the account.

You can identify account takeover by sudden changes in spending habits, login attempts from odd locations, or activity outside of ordinary work hours. Check for simultaneous login attempts from multiple devices; this could mean that stolen credentials are being utilized.

Account farming: Scammers produce a flood of fraudulent accounts, frequently with the use of automated bots, in order to take advantage of weaknesses in your referral, bonus, or loyalty programs. These accounts could swiftly drain any money you have put into your rewards programs.

If there is an unexpected increase in the creation of new accounts, especially from the same device or IP address, it could indicate account farming. Look out for accounts that don’t have much information about them or that do strange things, like claim bonuses too quickly.

Bonus abuse and referral fraud

Scammers exploit loopholes in your referral and bonus systems by making false accounts to claim these benefits repeatedly. This has the potential to seriously harm the efficacy and profitability of your reward programs.

Referral fraud may be present if accounts use similar or identical personal information, particularly when bonus claims are made many times. Do not trust accounts that are overly active and seem to be focusing just on claiming rewards.

Impact of new account fraud

Fresh account fraud has the potential to affect your company or financial institution in numerous important ways:

Financial losses for businesses

This is the part that will hit you the hardest:

- Stolen funds: Fraudsters can utilize fake accounts to drain your assets or take advantage of security holes in your systems to deposit their own.

- Unauthorized transactions: Fraudulent users may conduct illicit transactions from your company or wash their money through your system using fake accounts. Exacerbated losses happen to your finances if these purchases lead to chargebacks.

- Investigation and resolution costs: There are expenses associated with investigating and resolving fraudulent activities. To protect your business, you must identify questionable accounts, deactivate them, and possibly compensate affected clients.

Damage to brand reputation and customer trust

In more than one way, this can hurt your brand’s credibility and drain trust from customers:

- Loss of customer confidence: Clients may lose trust in your data security measures if they find signs of fraud on their accounts. As a consequence, customers become dissatisfied and less loyal.

- Negative publicity: If word gets out about a significant fraud, it could tarnish your reputation and result in inquiries from suspicious parties. This will significantly impact your ability to attract new clients.

- Reduced customer satisfaction: Deception can worsen consumer discontent and unhappiness. Some customers might be reluctant to do business with you again after an incident involving fraud.

Regulatory penalties for non-compliance

Strong rules pertaining to Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance affect financial institutions and other regulated businesses and, if not followed, could lead to regulatory fines.

Authorities could impose fines and penalties for inadequate actions taken to stop fresh account fraud. This can hurt your bottom line because these fines are big. Your capacity to operate or provide specific services may also be limited as a result of noncompliance.

Preventing new account fraud

To your relief, there are measures to reduce the likelihood of new account fraud. Here are a few important account fraud prevention tactics to think about, along with descriptions of how they function and the advantages they provide:

Identity verification

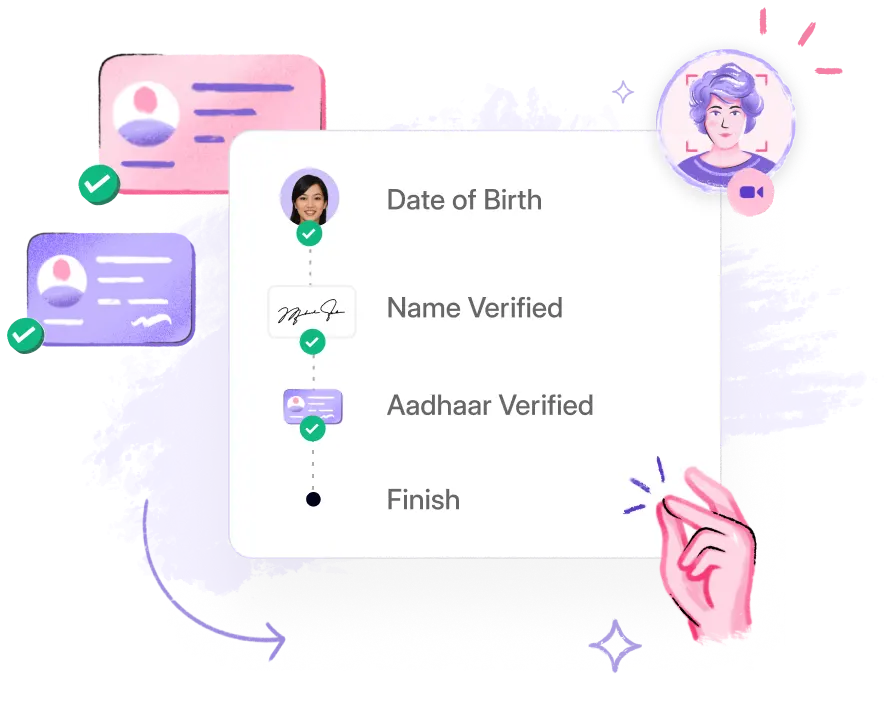

Collecting and verifying customer information: An important initial step in protecting your account creation fraud is collecting and verifying the information you provide when you create an account. This includes details like your name, address, date of birth, and government ID. Confirm the accuracy of this information by implementing verification mechanisms. In the first place, this might make it less likely that fraudsters will try to get false accounts. Making sure that only authorized users can access your system is one of the main goals of data verification. To put it another way, this safeguards your company from potential financial harm caused by fraudulent activities.

Using document verification and biometrics: Consider how biometrics and document verification techniques could help validate identification records. These instruments help to identify fraudulent account IDs and validate the account creator’s authenticity, therefore benefiting them. One can improve account security by linking biometric verification techniques—like facial recognition or fingerprint scanning—with a specific individual. Document verification and biometrics provide more gratification than merely compiling customer information. They can support the battle against advanced fraud and identity theft.

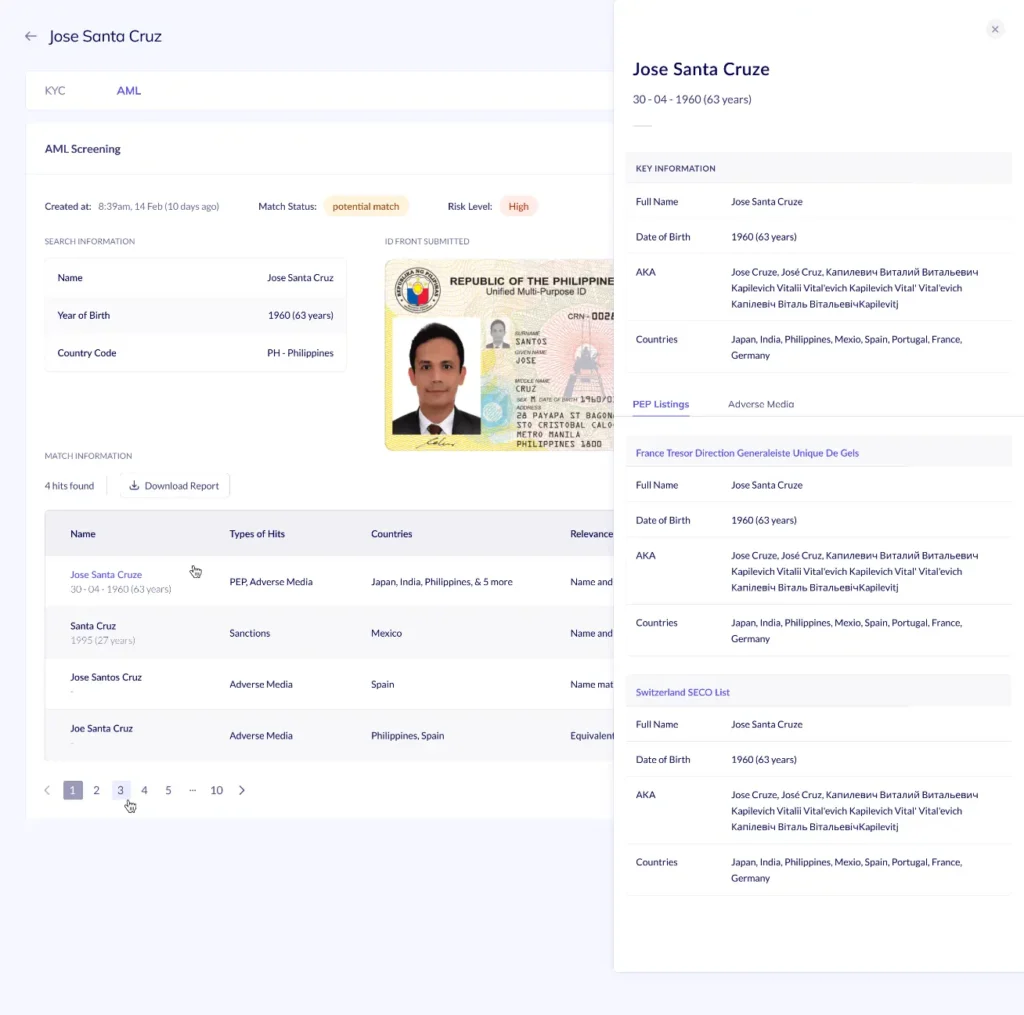

Implementing KYC and AML checks: KYC and AML regulations demand that businesses verify the identities of their clients and monitor any dubious activity. Following these rules reveals that you value serving your legitimate customers and stopping financial crime.

Transaction monitoring

Detecting suspicious activity and potential fraud: Put in place mechanisms to track bank account activity for anomalies pointing to possible fraud. This will help you find suspicious behavior. Something unusual could be occurring—a total change in spending patterns, money changing hands from an odd location, or something occurring outside of regular business hours.

Analyzing transaction patterns and user behavior: Using data analytics tools, examine behavior patterns and transaction patterns to find signs of fraud. Part of this process may include looking at things like IP addresses, device fingerprints, and normal user actions. One indicator of account fraud occurs when there is an increase in the number of attempts to create an account from the same device or IP address.

Risk-based approach

Assessing customer risk based on various factors: Different consumers present different levels of risk. Make a system that takes risk into consideration and uses it to prioritize accounts with a higher risk profile in terms of verification and monitoring. This might be determined by looking at things like the customer’s location, the sort of credit card account they are opening, or their transaction history.

Applying appropriate verification and monitoring measures: Apply the required actions to make sure your verification and monitoring processes match every client’s risk profile. High-risk accounts could be subject to extra security protocols, including biometric authentication, document verification, and ongoing transaction monitoring. Though they can still be checked regularly, lower-risk accounts may require fewer verification processes.

Staying ahead of fraud trends

Continuously updating fraud detection models: Criminals are always changing their strategies, so they must also be updated. Staying ahead of new threats requires frequently updating your financial fraud detection algorithms with the newest data and trends. If you want to do this, you need to expand your data set to include things like gadget specs or social media history.

Collaborating with industry partners and authorities: Exchange data and insights on how to prevent new account fraud with other companies in your field and with law enforcement. If you work with other people, you can pool their expertise to fortify your own defenses.

Conclusion

Although new account fraud poses a significant risk, it is feasible to overcome. You can safeguard your company and considerably lower the likelihood of fraud by employing a multi-layered method that incorporates strong identification verification, transaction fraud monitoring, and a system based on risk. Failure to remain watchful and to adapt to changing new account fraud prevention strategies will lead to failure in the long run.

HyperVerge has developed an extensive set of tools to assist companies like yours in the fight against new account fraud. Discover how HyperVerge can help your business in avoiding new account fraud by exploring our fraud prevention solutions.