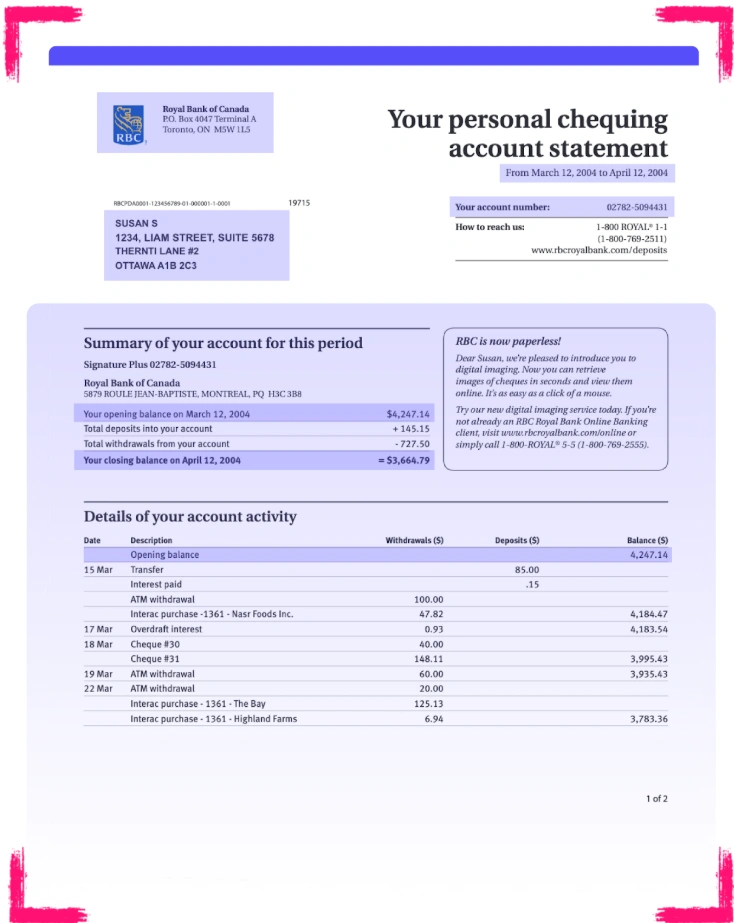

Most people check their bank balance, but few actually analyze their statements. Within those lines of numbers, lie the answers to better budgeting, smarter spending, and stronger financial security.

Living in a digital-first world makes personal bank statement analysis more relevant than ever. Understanding financial transactions is crucial for budgeting, loan approvals, and wealth management. With the rise of fintech, automated tools like HyperVerge streamline this process, offering accurate insights, fraud detection, and smarter financial planning—all with minimal effort.

What is personal bank statement analysis?

Personal bank statement analysis involves examining financial transactions. It aims to assess income patterns, expenses, and savings. This kind of analysis helps people stay on top of their budgets. It also helps them avoid unnecessary expenses, and improve their financial planning.

This analysis also helps individuals make informed financial decisions. Valuable insights into financial habits back these decisions. This can help create effective saving strategies and optimize cash flow management.

By understanding where money is coming from and where it is being spent, individuals can take better control of their finances. This helps them inch closer to their long-term financial security.

Why it matters in India

India is set to become a $1 trillion digital economy by 2028. This means, the digital financial ecosystem is growing at a rapid pace. With it, there’s a growing demand for loans, credit cards, and wealth management services. Fintech platforms, digital banking, and online lending services are on an all-time rise. Financial institutions use bank statement analysis to assess an applicant’s creditworthiness. Lenders check cash flow, spending patterns, and income consistency to determine loan eligibility.

Regular bank statement analysis goes beyond ensuring financial discipline. It also improves one’s credibility with banks and credit agencies. Digital payment methods such as UPI and mobile banking are also in the mainstream. This makes accurate bank statement analysis essential for financial literacy and security.

Why personal bank statement analysis matters

Effective personal bank statement analysis is crucial for managing finances with efficiency. Some of the key benefits include:

- Enhances budgeting and savings: Regular bank statement analysis helps track spending habits. It also identifies unnecessary expenses, and builds a better budget. Understanding your cash flow can help you make adjustments, improve savings and meet financial goals.

- Improves creditworthiness: Financial institutions assess bank statements to determine eligibility for loans and credit cards. A well-maintained financial record improves the chances of approval. This, in turn, reflects financial discipline and responsible money management.

By keeping an eye on spending patterns and maintaining a positive cash flow, individuals can better plan for large expenses, investments, or even emergencies.

How personal bank statement analysis works

Analyzing personal bank statements can be a tedious and overwhelming task. This is especially true for those unfamiliar with financial tracking. It’s easy to feel lost in a sea of numbers—given the several transactions, varying expense categories, and hidden fees. However, a structured approach can simplify the process. It can also provide valuable insights into financial health.

Key steps in the process

Here are three key steps to keep in mind while conducting a personal bank statement analysis:

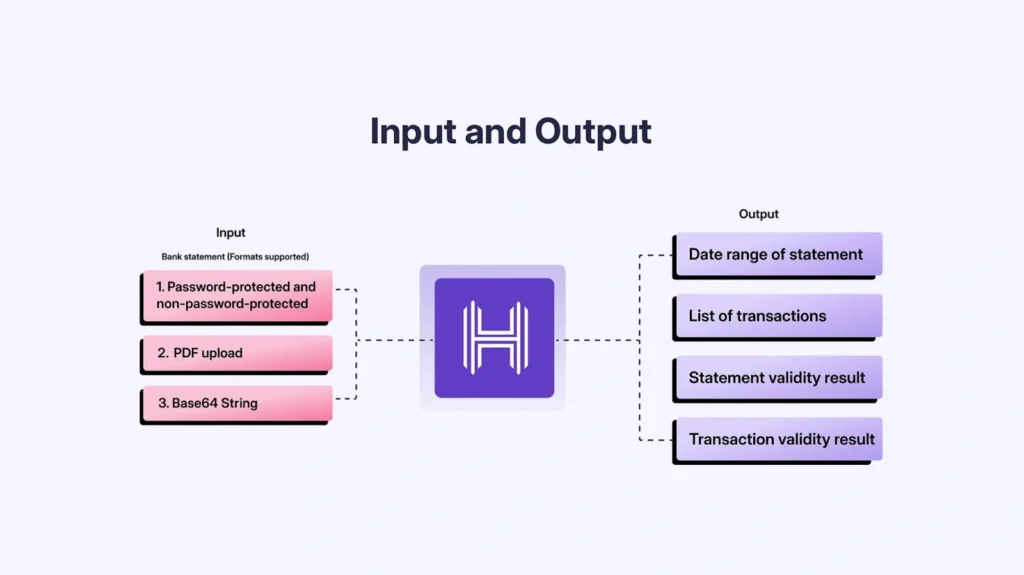

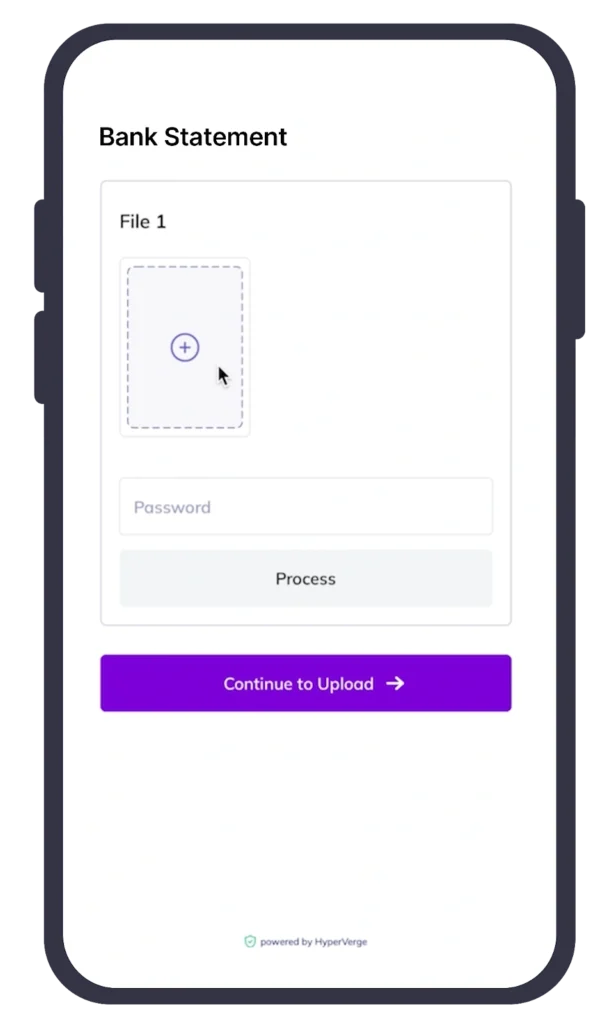

- Data extraction: Bank statements contain a wealth of financial data. Going through them manually can be time-consuming. Now, digital tools can extra data automatically from PDFs, CSVs, or direct bank integrations. Thus ensuring accuracy and efficiency.

- Categorization of transactions: Transactions are grouped into different categories. Like, income, fixed expenses (rent, EMIs, insurance), discretionary spending (dining, entertainment), and investments. Proper transaction categorization helps in understanding the financial flow. Besides, it also aids in budgeting and financial planning.

- Generating insights: Once transactions are categorized, individuals can generate insights into their spending behaviour, savings potential, and financial weaknesses. These insights help in making informed decisions about budget adjustments, investment planning, and financial growth.

Role of digitalization

AI and automation have transformed traditional bank statement analysis. Optical Character Recognition (OCR) and APIs enable real-time extraction, categorization, and insights. Digital tools improve accuracy and reduce errors. They inadvertently provide faster financial analysis compared to manual methods. With AI-driven insights, individuals can set realistic savings targets and detect unusual spending. Moreover, they can get automated recommendations for better financial management.

Using digital solutions ensures a hassle-free and data-driven approach to financial planning. Thus, allowing individuals to optimize their money management efficiently.

Challenges in traditional bank statement analysis

Traditional bank statement analysis methods have been in use for years. Experienced document analysts would review statements manually. However, a digitalised financial ecosystem means an increasing volume of transactions and innovative frauds. These have rendered manual methods obsolete. They often lack efficiency, accuracy, and timely insights, making financial decision-making more challenging.

Manual methods

Traditional methods of analyzing bank statements involved several manual steps. These include transactions, noting down expenses, and categorizing them. This approach is not only time-consuming but also prone to human errors.

Here are some common challenges:

- High volume of transactions: For businesses and individuals with frequent transactions, sifting through pages of bank statements can be overwhelming.

- Risk of errors: Missing or duplicate entries can lead to inaccurate financial assessments. These errors can impact budgeting and decision-making.

- Complex transactions: Financial instruments, foreign exchange dealings, and investment-related transactions can be difficult to interpret manually.

- Fraud detection challenges: Unauthorized or suspicious transactions—especially smaller ones—may go unnoticed without automated alerts.

Lack of real-time insights

Manual methods without automation lead to delays in financial insights. Thus making it difficult to make proactive financial decisions. Individuals may miss opportunities to optimize their savings. They may also fail to detect fraudulent transactions in time. Digital tools provide instant insights. They allow users to act quickly and make informed financial choices.

Benefits of digital tools for personal bank statement analysis

Digital tools have revolutionized personal finance management. They offer automated, precise, and real-time insights into bank statements. These tools eliminate the tedious process of manually sorting through transactions. They provide users with a clearer financial picture at a glance.

Whether you’re planning a monthly budget, preparing for a loan application, or optimizing your savings—digital tools are key. They streamline the process, ensuring accuracy and efficiency.

Accurate and fast financial insights

Manually analyzing bank statements is prone to human error and takes considerable time. Digital tools get rid of these inefficiencies by automatically categorizing transactions with precision.

AI-powered automation delivers real-time breakdowns of income, expenses, and savings patterns. This allows individuals to make quick financial decisions. Users can generate comprehensive financial reports without tedious calculations. They can accomplish these by simply pushing a button.

This accuracy guarantees that financial planning is based on factual data rather than guesswork. This, in turn, makes it easier to detect spending trends and anomalies.

Smarter budgeting and expense tracking

Managing money becomes easier when you have a clear view of your spending habits. Digital tools provide interactive dashboards. These are instrumental in identify spending trends and making adjustments in real time. Expenses are auto-classified into categories like rent, groceries, dining, and entertainment. This provides individuals with a clearer understanding of their financial health.

It also betters the ability to allocate funds to savings and investments efficiently. Additionally, some tools offer predictive analytics. They help users forecast future expenses and adjust their budgets proactively.

Real-time alerts and financial health monitoring

One of the biggest advantages of digital tools is real-time monitoring. Individuals receive alerts for unusual transactions, potential fraud, or upcoming bill payments. These alerts ensure that users stay informed about their financial status. They can take prompt action to prevent overdrafts, missed payments, or fraudulent activity.

Some advanced tools also analyze spending patterns over time and provide suggestions to improve financial health. Predictive analytics can even forecast future cash flow based on historical spending trends. Thus helping individuals stay financially prepared and avoid financial pitfalls.

Secure and compliant data handling

Security is a top concern when it comes to sensitive financial data. Compliance with industry regulations ensures that users’ personal and financial details are protected from unauthorized access or breaches.

Digital tools like HyperVerge use bank-grade encryption and comply with RBI regulations. This way, we ensure that users’ financial information remains safe and private. Besides, individuals have complete control over their data access. We ensure transparency and security while analyzing their bank statements.

With strict compliance measures in place, users can confidently leverage digital tools. They no longer have to harbour concerns about data misuse or privacy risks.

Best practices for personal bank statement analysis

Choosing the right tools

When analyzing personal bank statements, selecting the right digital tools is crucial. The ideal tool should prioritize three key criteria: accuracy, speed, and ease of use.

Accuracy is essential to ensure that the analysis reflects the correct financial details. Such as: transactions, balances, and recurring expenses. Speed is important for individuals and institutions looking for quick, yet thorough, insights. Tools that provide instant results can save time. They help users make decisions without delays.

Ease of use ensures that even individuals with minimal technical expertise can effectively analyze their statements without feeling overwhelmed. The tool should have the ability to adapt to different document layouts and styles. This is because different banks generate statements in different formats.

Be it a personal finance app or a specialized bank statement analysis tool—make sure it is intuitive, user-friendly, and capable of handling complex financial data.

Ensuring data security

Personal bank statements contain sensitive information. Hence, it’s essential to prioritize data security when choosing analysis tools. Secure platforms with encryption and privacy features should be non-negotiable. Encryption ensures that the data remains safe from unauthorized access during transmission and storage.

Furthermore, look for platforms that follow industry standards for data protection. Such as, GDPR or other local data privacy regulations. These tools should offer clear privacy policies. They must outline how your data will be used and stored. Users should feel confident that their personal information is being handled with the utmost care and security.

Educating users

It’s important to educate users on both the process and its advantages. Many individuals are unaware of the insights derived from analyzing bank statements. Educating users about the various benefits is key.

Additionally, users should understand how to interpret the information presented in the analysis. Clear, easy-to-understand reports and tools that offer educational support can make the process more accessible. Institutions offering these tools should also provide training or resources. This will guide users through the analysis process. In turn making it an empowering experience rather than a daunting one.

Takeaways

Personal bank statement analysis is a valuable tool. It’s instrumental in managing finances, making informed decisions, and understanding financial behaviour. From individuals seeking better budgeting to institutions assessing creditworthiness—adopting advanced tools can significantly enhance accuracy and efficiency.

As India’s financial landscape continues to evolve, adopting digital solutions like HyperVerge ensures efficiency, security, and better financial planning. Whether you’re tracking daily expenses or preparing for major financial decisions, we hold the key. Smart bank statement analysis empowers you to take control of your financial future.

For more information on how to improve your bank statement analysis, check out HyperVerge’s solutions here.