Can a bank statement say more about a person than their credit score?

It might sound odd at first, but the answer is yes. Credit scores tell you if someone missed a payment. Bank statements tell you why. They show patterns, how a person earns, spends, saves, and handles their everyday finances. For lenders, this kind of insight can be very useful.

In the U.S., more lenders are starting to look beyond traditional scores. They want to understand real financial behavior. The question is: can bank statement analysis really do that and do it well? Let’s take a closer look at how bank statements, tech, and customer behavior analytics are shaping up lending in the U.S.

What do we mean by ‘customer behavior’ in lending?

When lenders talk about ‘customer behavior,’ they’re simply looking at how a person manages their money over time. It goes beyond a credit score or a loan application form. It’s about the choices people make with their money–how they earn, how they spend, how often they repay on time, and how they handle financial ups and downs.

For example, does a person have a steady income? Do they spend carefully, or do they often run out of money before their next paycheck? Do they pay bills on time, or do they frequently miss deadlines? These small actions add up and tell lenders much more than a simple credit score can.

Traditional models, like FICO scores, only give part of the picture. They might show past mistakes, but don’t always reveal if someone has improved their habits. By looking at real financial behavior like consistent savings, responsible spending, or timely payments, lenders can make better, fairer decisions.

And now in 2025, lenders have even better ways to understand customer behavior. Through bank statement analysis APIs, customer behavior analytics, and advanced AI, they can spot patterns, habits, and risk signals much faster and more accurately. How does that work? We break it down below.

Bank statements: A hidden goldmine of behavioral data

Bank statements can tell you a lot more than just how much money someone has.

For lenders, they are full of small clues about how a person handles their day-to-day finances. Every deposit, withdrawal, bill payment, and shopping expense says something about the borrower’s habits. When looked at carefully, these patterns can help lenders understand a person’s financial behavior better than most traditional scores or documents.

For example, does someone get their salary on the same day every month? That shows income stability. Do they pay rent, phone bills, or EMIs on time? That points to responsible behavior. Do they regularly run out of money before the end of the month? That might signal poor money management or unstable income.

Read More: A Complete Guide to Bank Statement OCR

Even things like frequent cash withdrawals, gambling site transactions, or sudden large expenses can help lenders understand risk better.

This kind of detailed view is possible through bank statement analysis. With the right tools, lenders don’t have to read each line manually. They can quickly see trends like how much is spent on essentials vs. non-essentials, whether income is rising or falling, and how often there are penalties or overdrafts.

The best part? This data is real. It’s not self-reported or based on guesswork. Also, for lenders, using this data means they can make more accurate decisions. They can approve loans for people who might be rejected by traditional systems but show good financial habits. Or they can flag risky borrowers early.

Let’s now read how technology is changing the entire lending game in the U.S.

Want a clearer view of customer behavior?

HyperVerge’s Account Aggregators can help lenders access verified bank data securely, with customer consent. Schedule a DemoHow does technology turn transactions into actionable insights?

With the help of AI and machine learning, lenders can now scan and understand thousands of lines from bank statements in seconds. They spot things like frequent overdrafts, non-sufficient funds (NSF) charges, sudden drops in balance, or patterns of late-night spending.

Let’s say someone is a gig worker who drives for multiple ride-share apps. Their income might be unpredictable on paper. But AI can scan their account and see weekly deposits from different platforms, spot their busiest work seasons, and even detect how often they take breaks.

Tech also helps find warning signs. For example, if someone suddenly starts withdrawing large amounts of cash or their balance dips right after payday every month, that might raise questions about financial pressure or spending issues.

Read more:

The payoff: Why this matters for U.S. lenders?

Traditional models often miss important details. They can be unfair to people with little credit history or a few old mistakes. But behavior-based lending and customer behavior analytics are bringing in a more complete picture for U.S lenders; here’s how:

- Greater inclusion

Many people in the U.S. still struggle to access credit, not because they’re risky, but because they don’t have enough data to prove otherwise.

Young earners, gig workers, immigrants, or those who’ve never taken a loan often fall through the cracks. Behavior-based lending and customer behavior analytics can help close that gap. A clean bank statement with signs of responsible money habits can open doors for borrowers who were previously overlooked.

- Smarter credit decisions

When lenders rely only on credit scores or surface-level data, they may turn down good borrowers or approve risky ones. But behavior-based models look at how someone actually handles money, month after month. This helps reduce false positives (people who look good on paper but are high-risk) and false negatives (people with low scores but strong habits). It means fewer loan defaults and better portfolio health.

- Faster approvals

Behavioral data can be pulled and analyzed quickly, especially with the help of automation and smart tools. Instead of waiting days to manually check documents, lenders can now get a clear picture in minutes.

Patterns like regular income, on-time rent, and stable spending help speed up decisions. This saves time for both the lender and the borrower. Not to mention, faster approvals, happier customers, and lower costs.

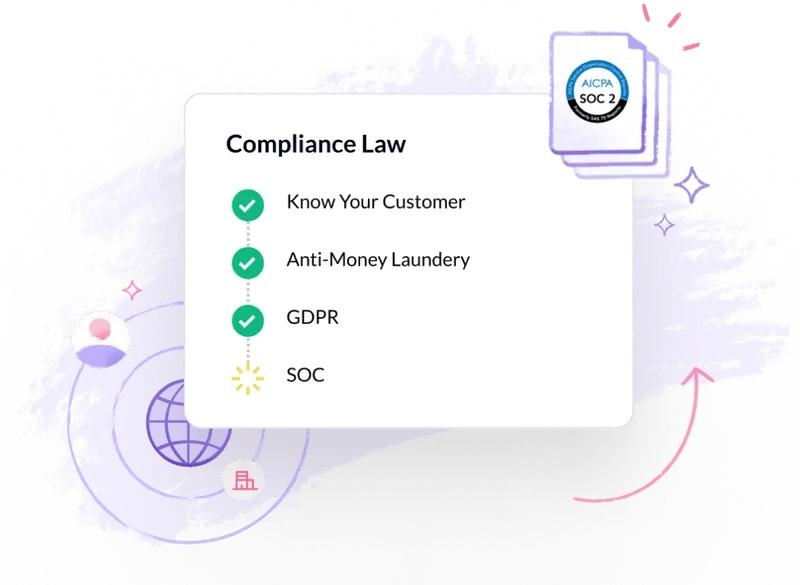

Compliance, privacy, and ethical guardrails

When lenders employ customer behavior analytics, especially sensitive information like bank statements, they can’t just use it any way they want. In the U.S. and beyond, both federal and state governments, as well as international authorities, have set clear boundaries. Let’s walk through them in plain language.

At the federal level, several laws (as mentioned below) set the tone for how lenders can collect, use, and share customer data:

| Law name | What it covers |

| Fair Credit Reporting Act (FCRA) | Limits how lenders collect and use credit and consumer data. Requires accuracy, clear purpose, and user consent. |

| Gramm-Leach-Bliley Act (GLBA) | Requires lenders to explain how they share customer data and to protect that data with proper safeguards. |

| Equal Credit Opportunity Act (ECOA) | Stops lenders from discriminating based on race, gender, age, or other personal traits. Applies to how behavioral data is used, too. |

| Truth in Lending Act (TILA) | Ensures lenders are transparent about loan terms and how data may affect decisions. |

These laws push lenders to be honest, careful, and fair. Even with powerful tech and AI tools, they can’t ignore these ground rules.

Now, some states go further than federal rules. One of the most well-known is California’s privacy law, which gives California residents the right to know what data is collected, ask for it to be deleted, and stop it from being sold. Applies even to behavioral data.

Other states like Colorado, Virginia, and Connecticut have passed similar privacy laws. Lenders working across states need to keep up with each one’s requirements.

Further, if a lender is working with global customers or using tools that process international data, they need to think beyond the U.S. One key law to know is the General Data Protection Regulation (EU) that gives people strong control over their data, requiring clear consent, the right to be forgotten, and limits on profiling.

Even U.S. companies without offices in Europe can be affected if they handle data from EU residents.

What’s next: The future of behavioral underwriting

Behavioral underwriting is moving from idea to action. Lenders are beginning to shift away from credit scores alone and are building systems that look at how people actually manage money. Instead of relying only on forms, past defaults, or outdated credit reports, future lending decisions will come from customer behavior analytics.

One big change HyperVerge sees is early risk assessment. With the help of embedded analytics, lenders will be able to assess borrowers quietly in the background, before a formal application even starts.

AI will also play a growing role. Instead of someone manually going through each line of a bank statement, AI systems can pull key insights, spot risks, and even interact with loan systems in real time. This won’t just save time, it will help reduce bias, flag edge cases, and make approvals more consistent.

But this only works if the tools are reliable. Not every data product is built for this level of detail. Lenders will need systems that don’t just extract data, but make sense of it, and do so in ways that are easy to understand and explain.

Do remember: behavioral underwriting isn’t about replacing people. It’s about helping lenders see more clearly and make faster decisions through the power of technology and customer behavior analytics.

Wrapping up: From statements to smarter lending

Spending habits, savings patterns, and payment behavior can all give clues about risk and return, far beyond what a credit score or basic form might reveal. When lenders tap into this kind of real-world behavior, they make sharper decisions. They avoid false negatives. They include more people. And they move faster.

For U.S. lenders, this shift is a chance to move past outdated models. Customer behavior analytics isn’t a nice-to-have anymore; it’s becoming a must. The most forward-thinking lenders are already building it into their systems and rethinking how they approve and underwrite.

If you’re looking to get started, HyperVerge makes it easier. In line with global data practices, the bank statement analysis solution pulls insights directly from raw bank data, helping you detect patterns, flag risks, and make sense of financial behavior quickly and clearly.

Unlock the power of behavioral insights. Book a demo with HyperVerge today.

FAQs

1. What is customer behavior analytics?

Customer behavior analytics is the process of studying how customers interact with a business. This includes analyzing actions like browsing, purchasing, and providing feedback. By understanding these behaviors, businesses can improve customer experiences, tailor marketing strategies, and predict future customer needs.

2. What are the 4 types of customer behavior?

There are four main types of customer behavior:

- Complex buying behavior: Occurs when customers are highly involved in a purchase and display significant differences among brands. This is common with expensive or infrequent purchases.

- Dissonance-reducing buying behavior: Happens when customers are highly involved but see little difference between brands.

- Habitual buying behavior: Characterized by low involvement and few perceived brand differences. Customers buy out of habit, often choosing the same brand without much thought.

- Variety-seeking buying behavior: Occurs when customers have low involvement but perceive significant differences among brands. They often switch brands for the sake of variety.

3. What 4 pieces of information does a bank statement tell you?

A bank statement gives a clear view of how money moves in and out of your account. Here are four key things it shows:

- Deposits and withdrawals: You can see all the money that has come in (like salary or refunds) and gone out (like bill payments or purchases).

- Transaction dates and details: Each entry includes the date and usually a short description of who or what the money was for, helping you track your spending.

- Balance information: The statement shows your starting and ending balance, along with the balance after each transaction, so you can see how your money changed over time.

- Bank and account information: It includes basic details like your account number, statement period, and sometimes contact details for the bank, which can be helpful for record-keeping or if you spot an error.